Six Answers for Small and Solo Businesses about Health Insurance

Tax PlanningIn this article, we answer some additional questions that will benefit small and solo-owned businesses, including:

- What steps do I take to properly reimburse 105-HRA expenses?

- Can my 105-HRA reimburse and deduct Medicare payments (both mine and my spouse’s)?

- Can you show me a big-picture flowchart of who can participate in a 105-HRA?

- How do we, as 50-50 owners of an S corporation, find qualifying insurance and deduct it?

- How do spouses that operate a 50-50 LLC deduct health insurance for the employee-spouse?

- Can I consider the Medicare tax a cost of insurance for the 105-HRA plan?

Question 1

My husband works for me occasionally. I have set him up with the 105-HRA plan with family coverage. I think I have most of this figured out, but I am confused on how the reimbursement works when I go to the store and use my personal credit card to buy my prescription. Can you explain the process to me?

Answer 1

Sure. Remember, your husband is the employee. You are covering him with a 105-HRA family plan.

To make this crystal clear to an IRS examiner, do this:

- Using your business checking account, reimburse your employee-husband for 100 percent of the medical expenses.

- Require your employee-husband to submit the medical expense receipts to you monthly.

Now, let’s go pick up your prescription. You paid for the prescription with your personal credit card. How does this work with the reimbursement?

You have two choices:

- You can give the receipt to your employee-husband, who can submit it to your business for reimbursement to him.

- Your husband could write you a personal check for the cost of the prescription and then submit the receipt and canceled check for reimbursement.

Note that in both cases, you use your business checking account to reimburse your employee-husband for your prescription.

Question 2

My spouse and I are both insured by Medicare. Is the cost of Medicare includable in a 105-HRA medical reimbursement plan?

Answer 2

Yes, with the 105-HRA family medical plan, both Medicare premiums and any supplemental insurance plans are reimbursable by the plan and thus deductible by the business.

Again, as with question 1, you want to reimburse the premiums to the employee-spouse.

Question 3

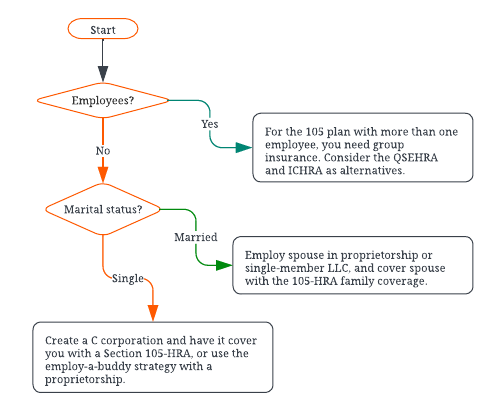

Do you have a big-picture flowchart to help me understand who qualifies for the 105-HRA plan and who does not?

Answer 3

We do now. See below:

With the buddy strategy, you (as a Schedule C taxpayer) hire your buddy as your one and only employee, and cover the buddy with the 105-HRA plan. In return, your buddy uses his or her proprietorship to hire you and cover you with a 105-HRA plan.

Question 4

My business partner and I began operating our business as an S corporation in August 2021. We are 50-50 owners and take equivalent wages and distributions.

Our insurance company tells us that we are not eligible for their health insurance coverage. What is the best way for us to set this up, considering that each owner wants health insurance?

Answer 4

First, you might check with other health insurance companies to see if they have plans that would cover you and your fellow shareholder as employees of the S corporation.

Regardless, here’s good news: You don’t need group insurance. You and your fellow shareholder can buy individual coverage, and the S corporation can reimburse you for the premiums.

The results you achieve with the individual purchases of insurance are identical to what you would have had with group insurance. It works like this:

- You and your fellow shareholder submit expense reports with the premiums to the S corporation, which the corporation reimburses.

- The S corporation puts the reimbursements on your W-2s in box 1, but not in box 3 or box 5.

- You and your fellow shareholder deduct the premiums as self-employed health insurance on Schedule 1 of your Form 1040, assuming that your box 5 wages exceed the cost of the insurance and that you otherwise qualify for the deduction.

Question 5

My spouse and I live in Washington state. We have 50-50 ownership in the LLC that we use to operate our business. I am the primary worker in the business. Can I hire my spouse on a part-time basis and take advantage of the 105-HRA?

Answer 5

First, know this: you and your spouse can “elect” to treat your partnership LLC as a single-member LLC because you and your business reside in a community property state.

Once you elect single-member LLC status, you can hire your employee-spouse as your one and only employee and cover him or her with a family 105-HRA plan.

For those who don’t live and operate in a community property state, you need to rid yourselves of the multi-member LLC and operate as a single-member LLC or as a proprietorship.

Question 6

As you know, the feds take Medicare tax money from my W-2 and from my S corporation. Can the S corporation reimburse me for the Medicare taxes I paid to the feds and treat that as a payment for health insurance?

Answer 6

Nice try, but as they say, “No dice.” Without question, you used what would appear to be good logic. Unfortunately, you are dealing with the tax law here, and the feds’ extraction of Medicare taxes from your W-2 is not a payment for your health insurance. It’s simply a tax.

Takeaways

For the 105-HRA family plan, reimburse your employee-spouse for 100 percent of your family’s medical expenses, using your business checking account. Have your employee-spouse submit a request for reimbursement monthly that includes receipts.

For ideas on when the 105-HRA plan works, see the flowchart in this article.

S corporation owners can purchase individual health insurance coverage and have the corporation reimburse the premiums. The reimbursements are then reported in box 1 of the W-2, but not in box 3 or 5.

If you live in a community property state, you and your spouse can elect to treat your partnership LLC as a single member LLC. This allows you to hire your spouse as an employee and cover him or her with a family 105-HRA plan.

Medicare taxes extracted from your W-2 are not considered health insurance payments and cannot be reimbursed as such by an S corporation.